Income Tax Calculator (New Tax Regime)

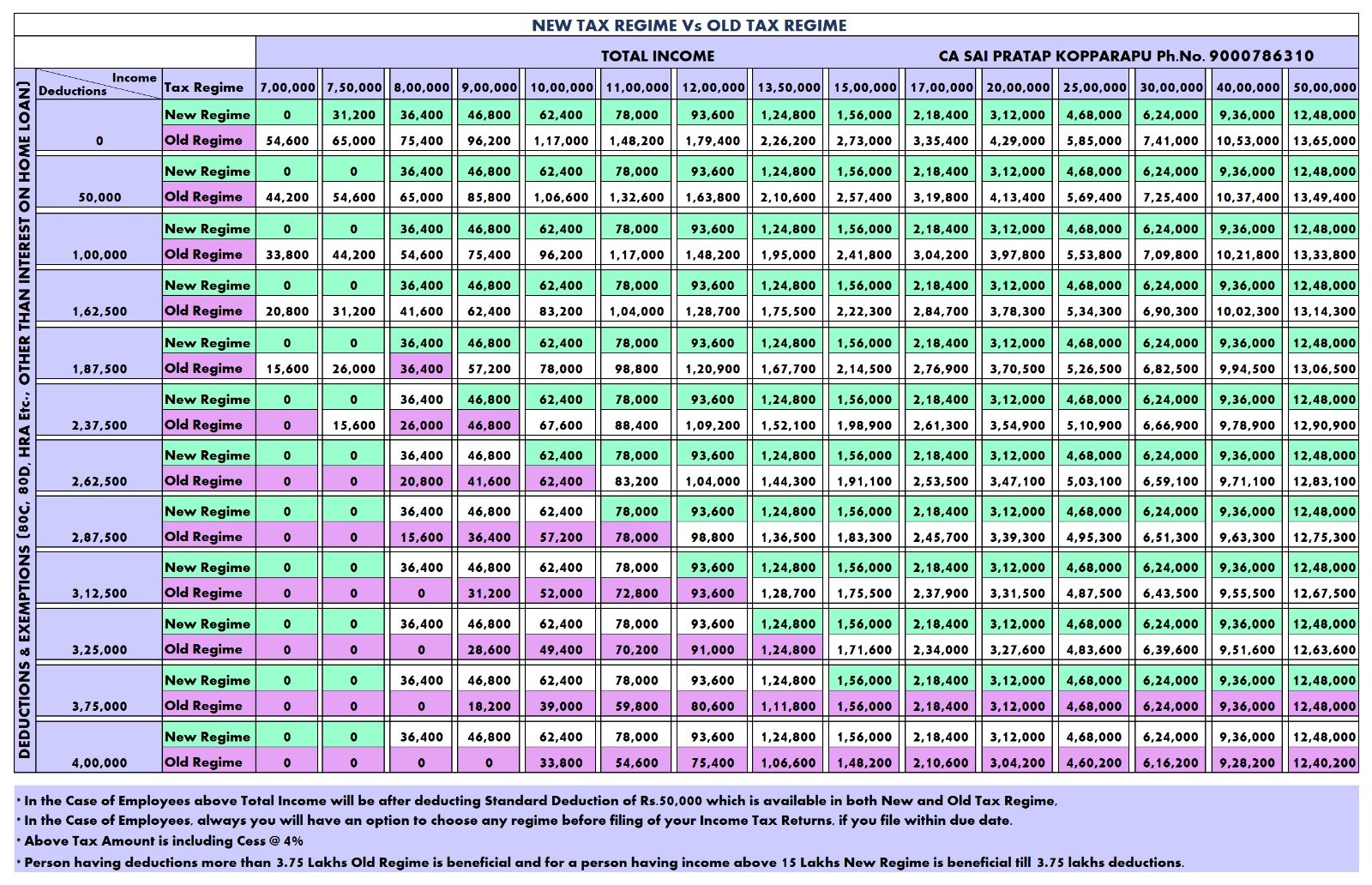

* For salaried employees, standard deduction of Rs. 50,000 can be deducted from the Gross Salary to arrive the Taxable Income. Additionally, taxable income includes other earnings such as interest from savings bank accounts, fixed deposits, and also from other heads of incomes.

All you need to know about New Tax Regime:

The Income Tax slab rates for the new tax regime, applicable to Individuals and HUFs for the Assessment Years 2024-25 and 2025-26, are as follows:

| New Tax Regime | |

|---|---|

| Taxable Income | Tax Rate |

| Up to Rs. 3 Lakh | Nil |

| 3 Lakh to 6 Lakh | 5% |

| 6 Lakh to 9 Lakh | 10% |

| 9 Lakh to 12 Lakh | 15% |

| 12 Lakh to 15 Lakh | 20% |

| Above 15 Lakh | 30% |

Benefits of the New Tax Regime:

- Standard deduction of ₹50,000 for salaried employees.

- Attractive tax rates compared to the Old Tax Regime.

- No need to invest in Life Insurance, Health Insurance, PPF, Home Loans, etc., to save taxes.

- Zero tax for individuals with a total income up to ₹7 lakhs or salary up to ₹7.5 lakhs.

- Deduction to the extent of 2 lakh on Home Loan Interest paid on the property given on rent.

- Deductions for NPS contributions, gratuity, leave encashment, and contributions to the Agniveer Corpus Fund.

- Transportation allowance deduction for differently-abled individuals from salary.

- Tax exemption for Voluntary Retirement Scheme.

- Standard deduction for family pension up to ₹15,000 or 1/3rd of the pension amount, whichever is lower.

Capsule: Even if you have opted for New Tax Regime in your company, still you have option to switch the regime based on the tax savings while filing your Income Tax Returns only when you file within the due date of filing original returns, generally within 31st July.

Understanding the New Rebate Under Section 87A in the New Tax Regime

Overview of Section 87A Rebate:

In the Old Tax Regime, the Section 87A rebate is available only to individuals with taxable income of up to Rs. 5 lakhs. However, in the New Tax Regime, this rebate is extended even to those with taxable incomes exceeding Rs. 7 lakhs. This change introduces a concept similar to Marginal Relief for Surcharge, designed to prevent individuals from facing a steep tax increase due to minor income increments.

Key Points of the New Rebate System:

- Rebate Applicability:

- Old Tax Regime: Rebate under Section 87A is available only if the taxable income is Rs. 5 lakhs or less.

- New Tax Regime: The rebate is now applicable to individuals and HUFs with taxable income exceeding Rs. 7 lakhs, providing a marginal relief for those with incomes just above this threshold.

2. Illustrative Examples:

Situation 1: Mr. Amit’s Scenario

Illustrative Examples:

Situation 1: Mr. Amit’s Scenario

| Taxable Income | 7,00,000 |

| Tax on Above (New Regime) | 25,000 |

| Rebate u/s 87A | 25,000 |

| Tax Payable | Nil |

Situation 2: Mr. Varun’s Scenario

| Taxable Income | 7,10,000 |

| Tax on Above (New Regime) | 26,000 |

| Rebate u/s 87A | – |

| Tax Payable | 26,000 |

3. New Rebate Mechanism:

Calculation Adjustment:

As per the new rebate concept, tax payable by Mr Varun will be limited to the taxable income he earned in excess of Rs.7 Lakhs i.e., Rs.10,000 (7,10,000- 7,00,000)

Therefore, the rebate will be the difference between actual tax and tax payable as mentioned above, i.e., Rs.26,000 less Rs.10,000 = Rs.16,000

| Taxable Income (A) | 7,10,000 |

| Tax on Above (B) | 26,000 |

| Taxable Income in Excess of Rs.7 Lakhs (C = A – 7,00,000) | 10,000 |

| Tax Payable (D = Lower of B and C) | 10,000 |

| Rebate u/s 87A (E = B-D) | 16,000 |

4. Threshold for Rebate:

- For incomes exceeding Rs. 7,27,775, the rebate under Section 87A becomes Nil.

Conclusion: This adjustment ensures that taxpayers like Mr. Varun, who earn just above the Rs. 7 lakh threshold, are not unduly penalized. The new system maintains fairness, allowing a reasonable tax burden relative to income increments.

Useful Links:

1. Tax Comparision Calculator in Excel Format – click here to Download

2. Tax Comparision Illustration – click here to Download

{kind=link}

3. New Tax Regime vs. Old: Which One Saves You More on Taxes?

Author:

Sai Pratap Kopparapu

Chartered Accountant | Registered Valuer (SFA)

For further queries, you can reach us: ca.saipratapk@gmail.com